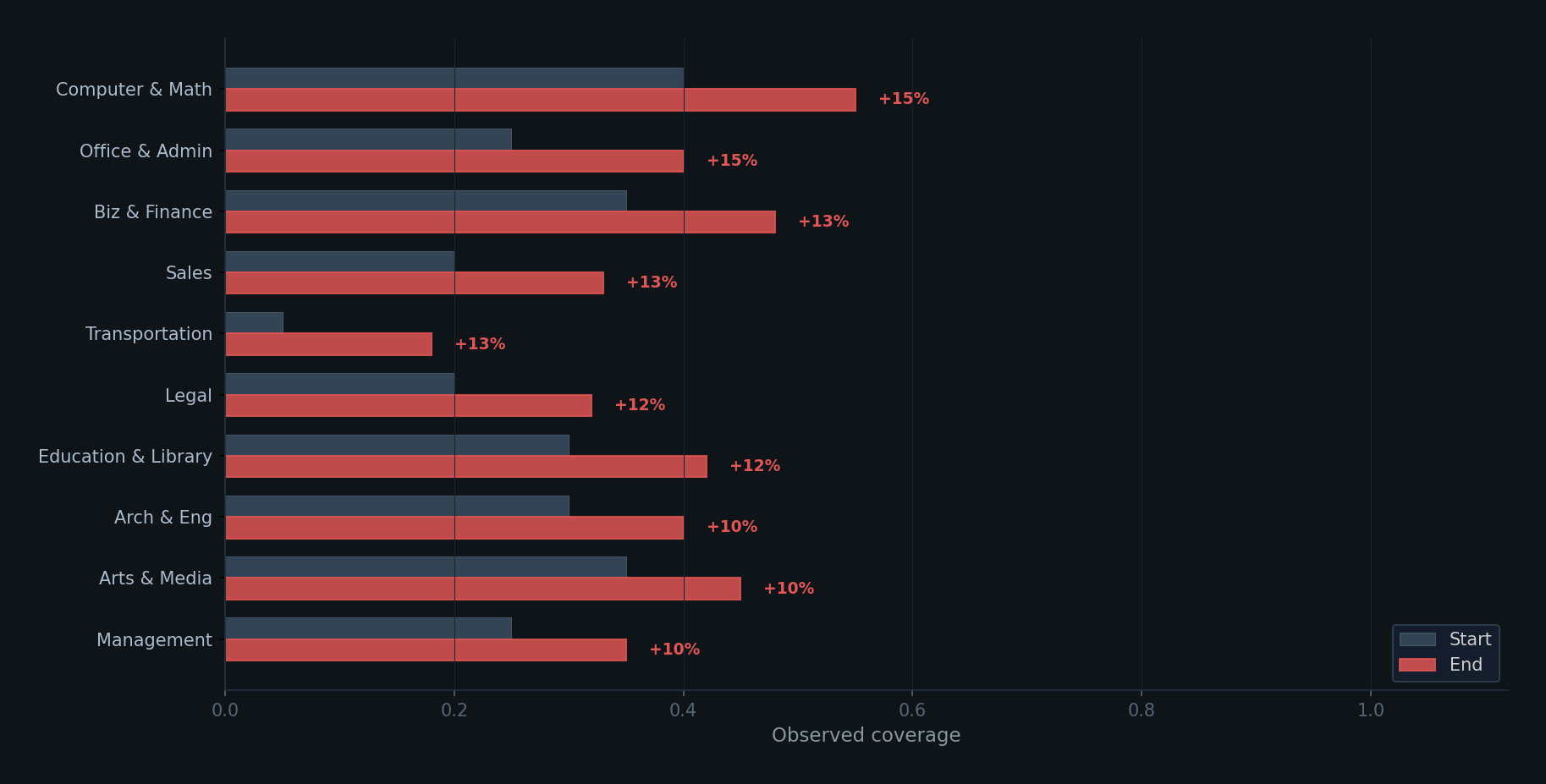

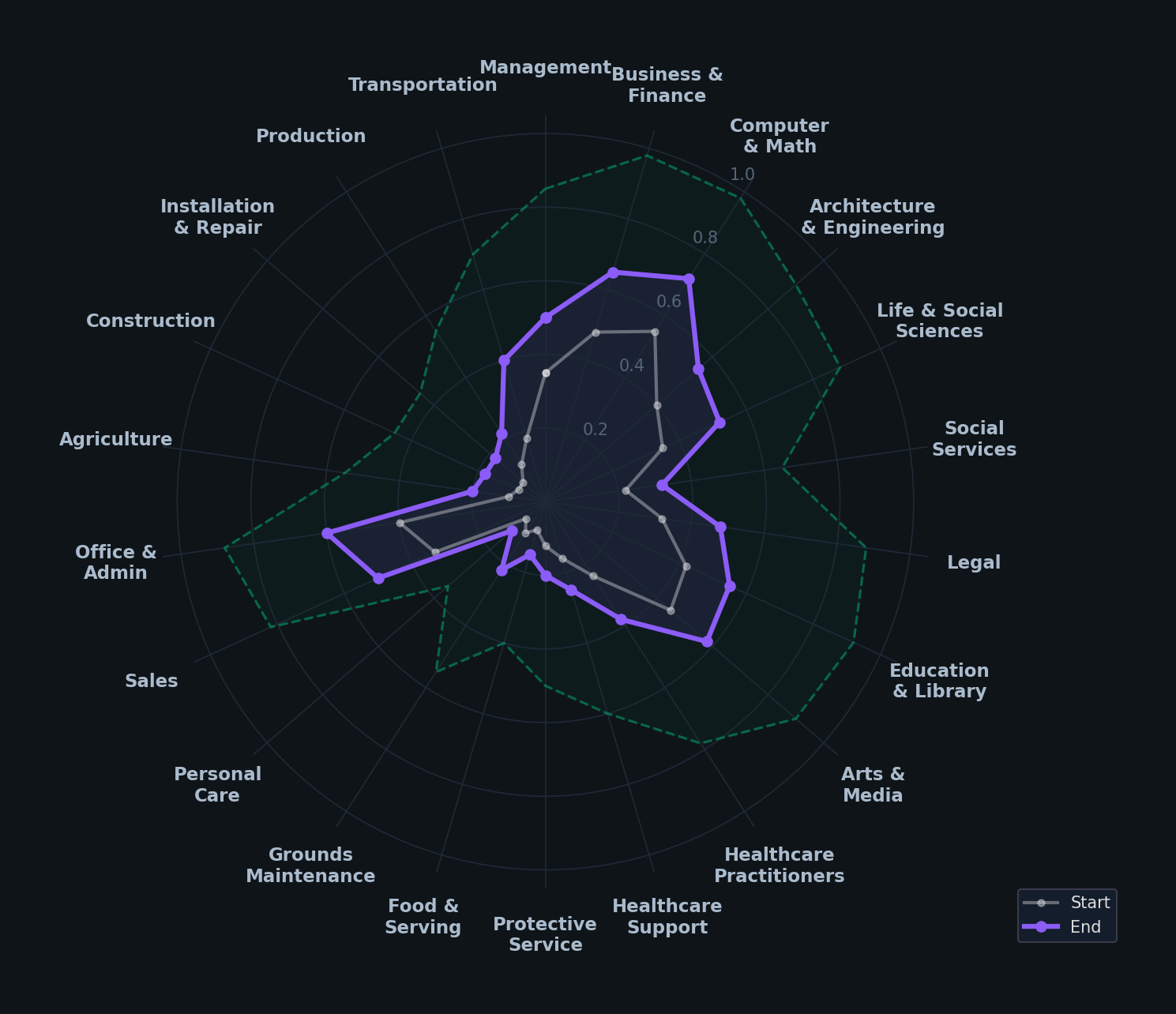

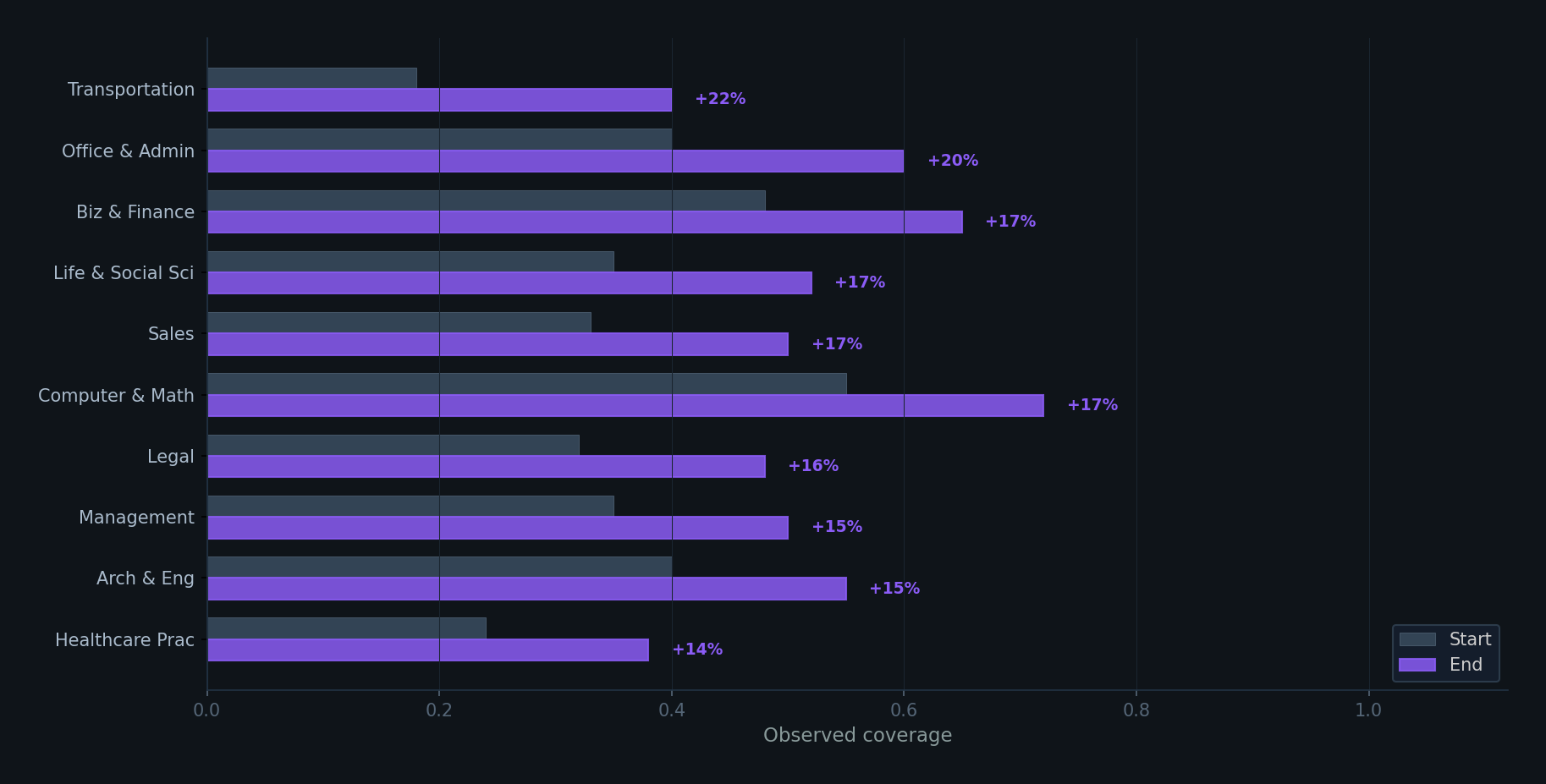

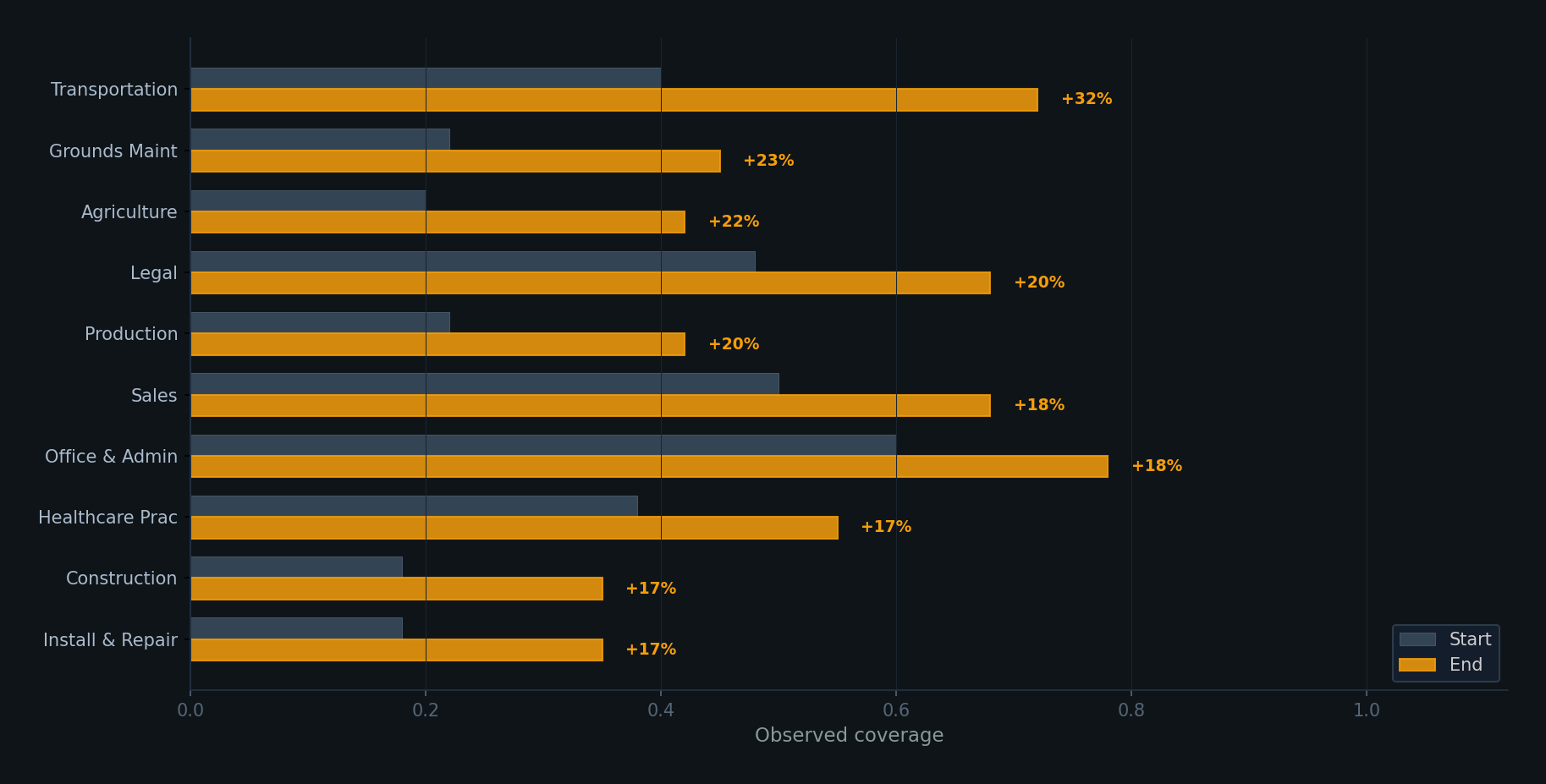

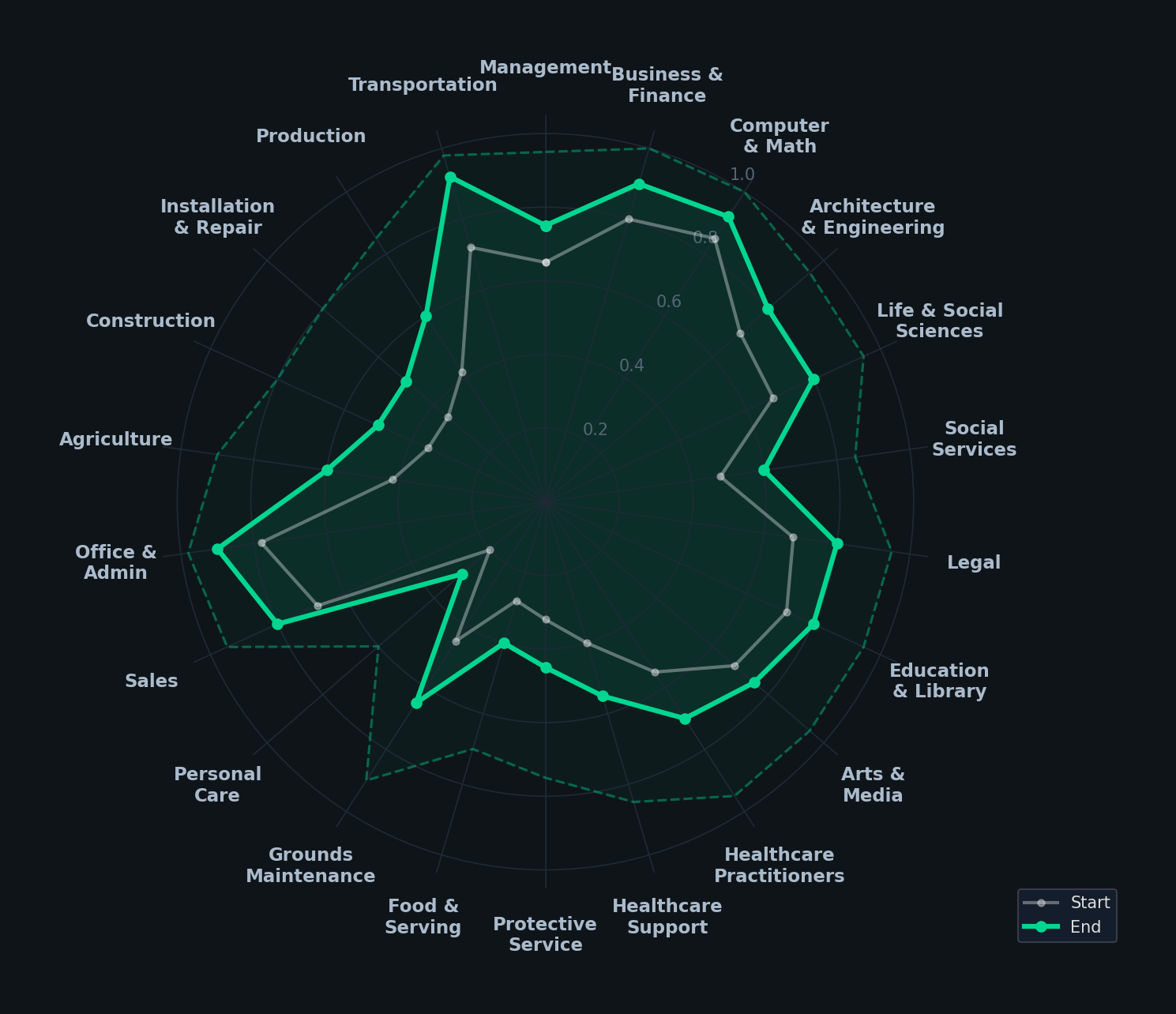

There's a radar chart that maps AI coverage across 22 occupational categories - everything from computer science to construction, legal to landscaping. It plots two lines: theoretical capability (what AI could handle if we let it) and observed adoption (what's actually deployed in the real world).

In 2024, those two lines tell a dramatic story. The theoretical coverage is already massive in knowledge work - computer & math at 0.95, business & finance at 0.95, architecture & engineering at 0.85. AI could already do most of this work.

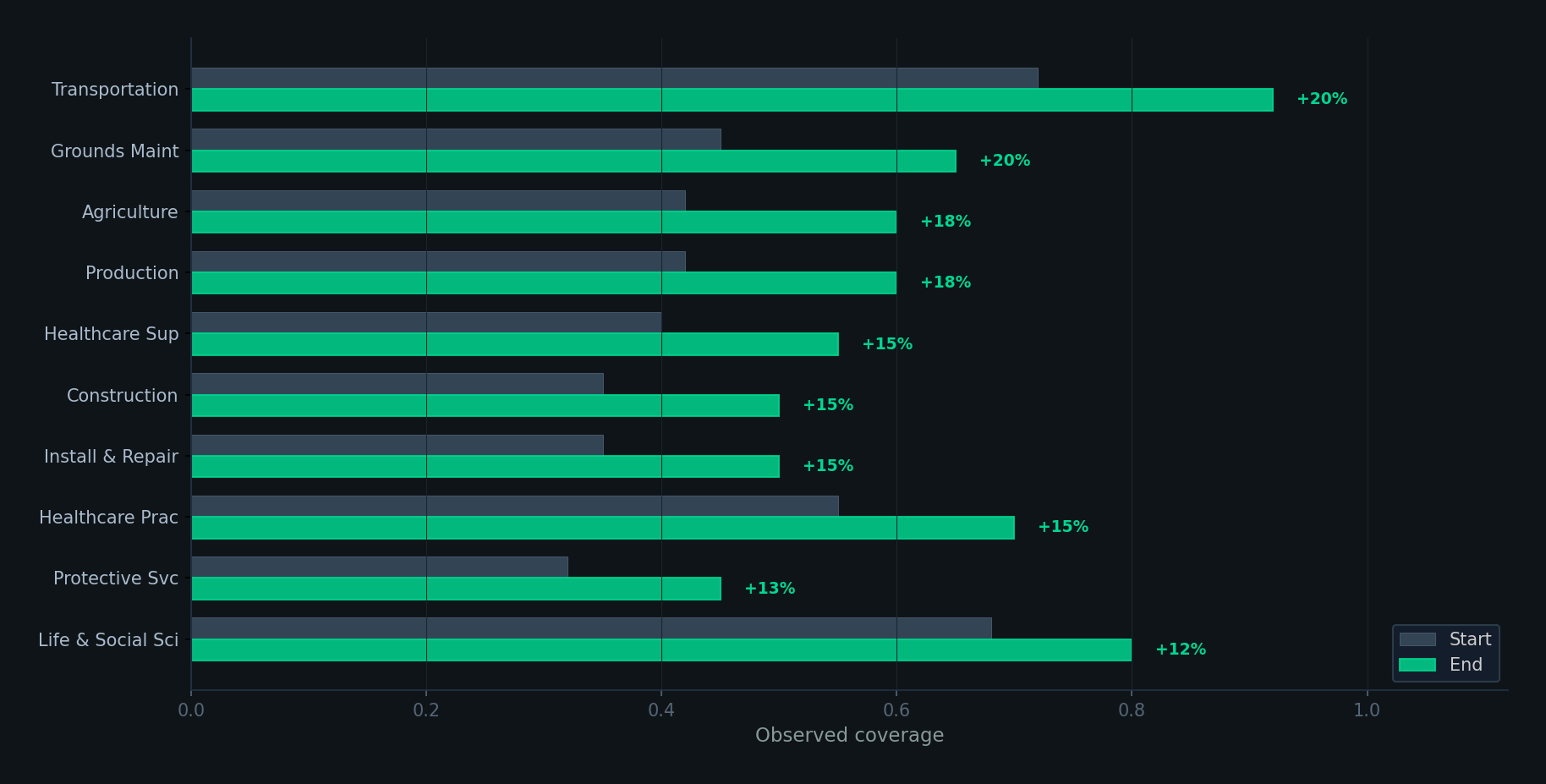

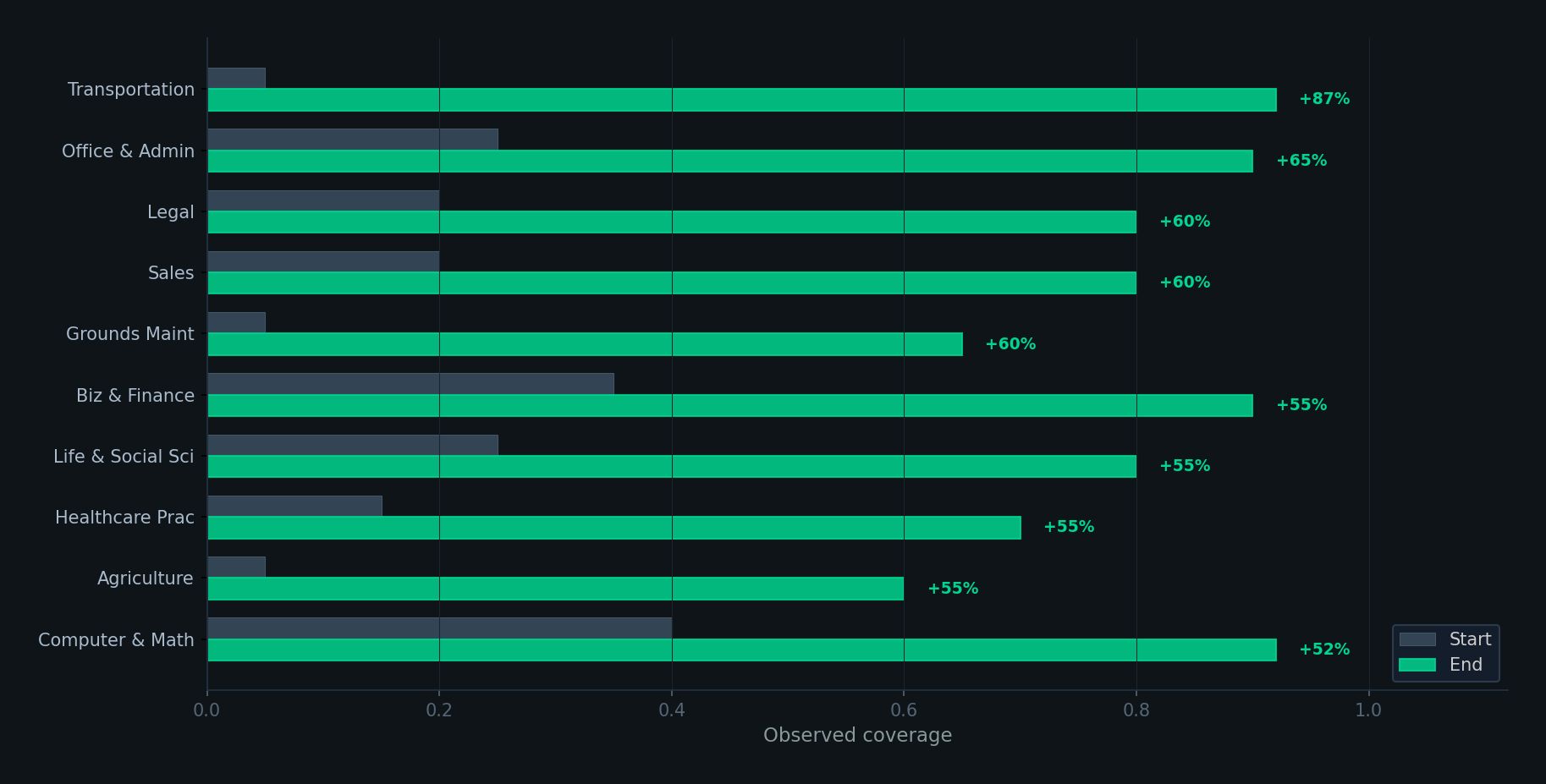

But observed adoption? It's a tiny cluster huddled in the center of the chart. Computer & math at 0.40. Business & finance at 0.35. Legal at 0.20. And anything requiring a physical body - construction, agriculture, installation & repair - is sitting at essentially zero.

That gap between “can” and “does” is the adoption curve. And it's about to go exponential.

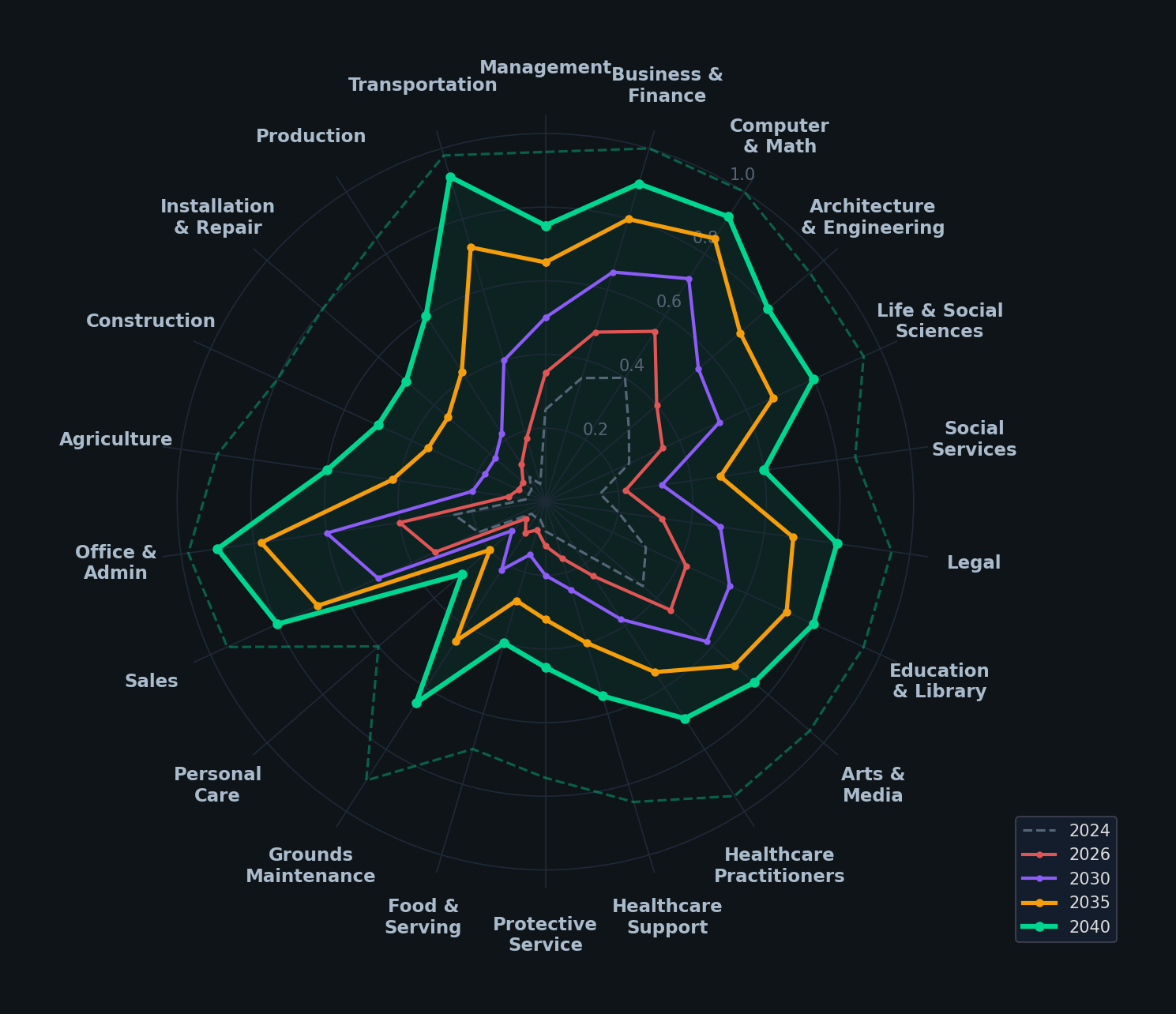

I projected this forward by modeling the convergence of three forces: AI (software intelligence), robotics (physical execution), and nanotechnology (molecular-scale precision). Each one compounds the others. Here's the map, era by era.